Why Do Variances Stop Being Useful (and What Does That Signal About Your Cost System?)

Variance analysis is supposed to be one of the most powerful tools in a manufacturing business. It highlights changes, surfaces issues, and drives corrective action. But in many companies, variances are still reported—yet no longer useful. Variances stop being useful when the underlying standards are no longer aligned with operational reality. When that happens, variances […]

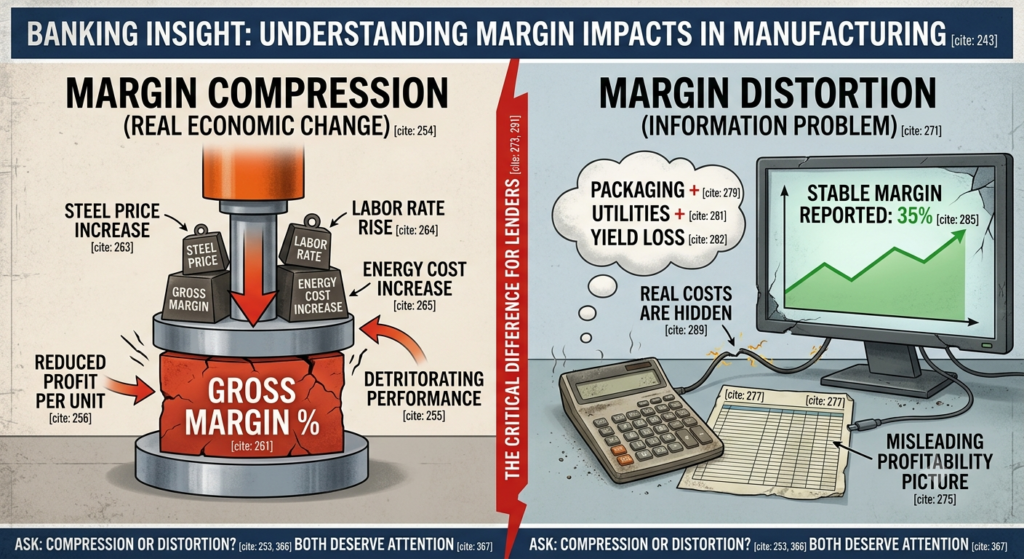

Margin Compression vs. Margin Distortion: Which One Creates Greater Risk for Commercial Bankers?

Direct Answer Margin compression and margin distortion are not the same problem, even though they can produce similar financial results. Margin compression occurs when the actual economics of a manufacturing business deteriorate because costs increase or pricing weakens. Margin distortion occurs when the costing system no longer accurately measures profitability. For commercial bankers, distinguishing between […]

Why Do Manufacturing Gross Margins Sometimes Stop Reflecting Reality?

Direct Answer Yes. Manufacturing gross margins can appear stable or even improve while actual production economics deteriorate. This occurs when standard costs, inventory valuation methods, overhead allocations, or production assumptions fail to keep pace with operational reality. Commercial bankers who rely solely on reported margins may miss early signs of weakening earnings quality, cash flow […]

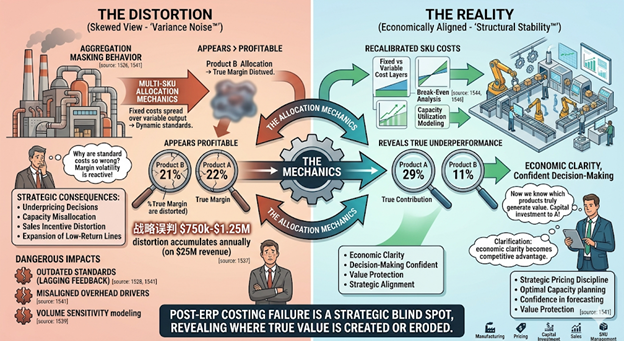

What Is Cost Signal Distortion in Manufacturing Financial Reporting?

Cost Signal Distortion™ occurs when internal financial reports communicate signals thatappear precise but are economically misleading due to structural misalignment in thecost system. This distortion arises when standards, overhead allocation drivers, absorptionmechanics, or inventory valuation logic no longer reflect how production resources areactually consumed. The accounting system continues functioning correctly, but thesignals executives rely on […]

What Is Volume Sensitivity Exposure in Manufacturing Cost Systems?

Volume Sensitivity Exposure™ is the degree to which gross margins change as production volume fluctuates under a fixed overhead absorption structure. Because fixed costs are spread across the number of units produced, changes in production volume alter the per-unit cost even when operational performance remains unchanged. As a result, margin volatility may reflect structural cost […]

What Is Contribution Illusion in Manufacturing Cost Systems?

Contribution illusion occurs when a product, customer, or division appears profitable under existing cost allocation mechanics but becomes significantly less profitable once overhead drivers are aligned with actual operational behavior. This distortion typically develops when overhead allocation methods fail to reflect how production resources are truly consumed. The accounting system continues producing accurate financial statements, […]

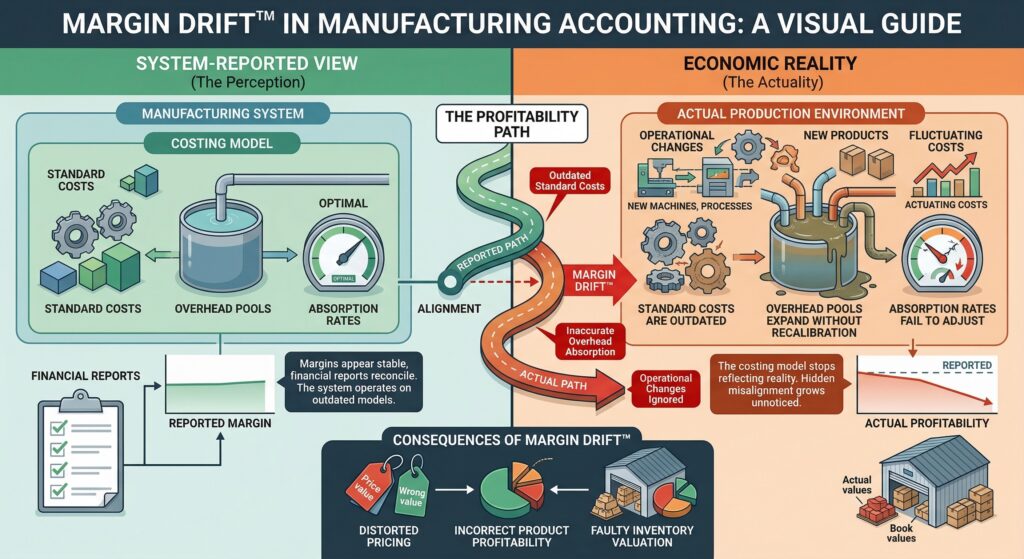

What Is Margin Drift in Manufacturing and Why Do Most Companies Miss It?

Margin drift occurs when the costing model inside a manufacturing system gradually stops reflecting how production actually behaves. Standard costs become outdated, overhead pools expand without recalibration, and absorption rates fail to adjust to operational changes. Financial reports may still reconcile and margins may appear stable, but the reported profitability slowly separates from economic reality. […]