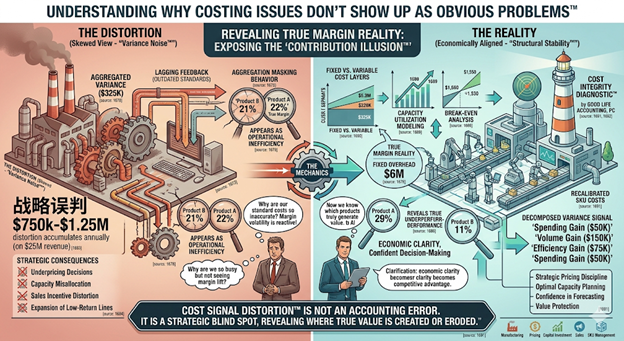

Why Don’t Costing Issues Show Up as Obvious Problems?

Most manufacturing leaders assume that if something is wrong with their costing system, it would be obvious. Margins would drop.Inventory would spike.Financial results would clearly signal a problem. But that’s not how costing issues behave. Costing issues rarely show up as obvious problems because they develop gradually, spread across multiple areas, and are often masked […]

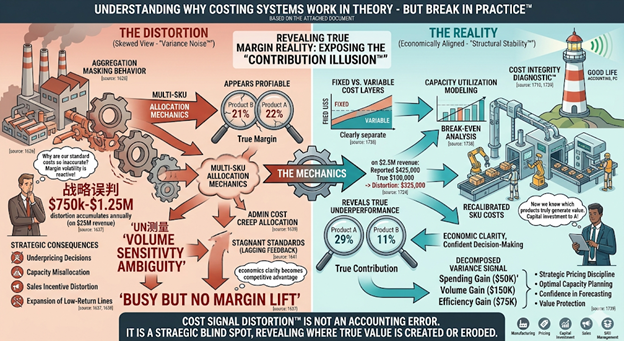

Why Does Your Costing System Work in Theory—but Break in Practice?

A costing system works in theory but fails in practice because it reflects assumptions—not actual operational behavior. Over time, production realities shift while cost structures remain static, creating hidden distortions in margins, inventory, and decision-making. What appears “accurate” in reports is often misaligned with how costs truly flow through the business. Costing Systems Are Built […]

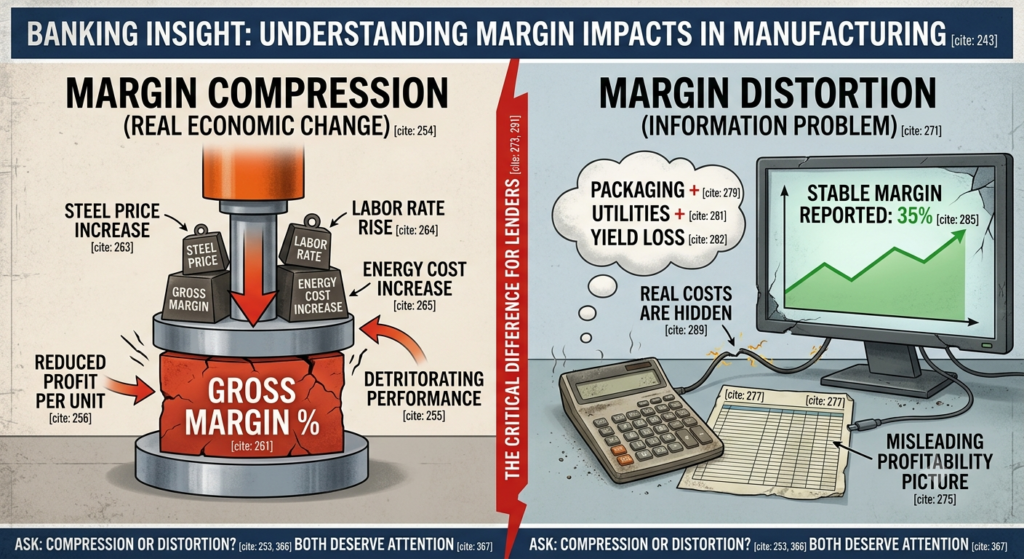

Margin Compression vs. Margin Distortion: Which One Creates Greater Risk for Commercial Bankers?

Direct Answer Margin compression and margin distortion are not the same problem, even though they can produce similar financial results. Margin compression occurs when the actual economics of a manufacturing business deteriorate because costs increase or pricing weakens. Margin distortion occurs when the costing system no longer accurately measures profitability. For commercial bankers, distinguishing between […]

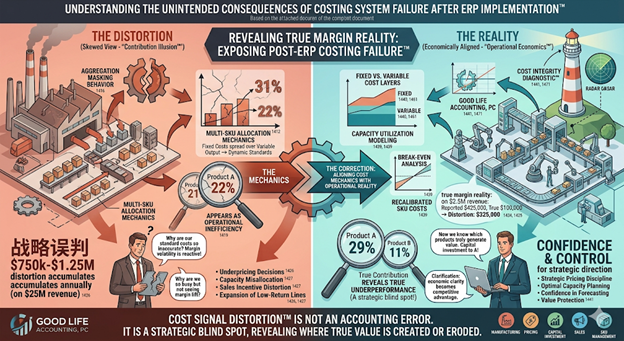

Why Do Costing Systems Fail After ERP Implementation?

ERP systems are designed to bring structure and control to manufacturing operations. But many companies discover—often too late—that their costing problems didn’t disappear after implementation. In some cases, they got worse. Costing systems fail after ERP implementation because ERP systems configure structure—not cost accuracy. If cost drivers, standard costs, and operational assumptions are not validated […]

Why Do Manufacturing Gross Margins Sometimes Stop Reflecting Reality?

Direct Answer Yes. Manufacturing gross margins can appear stable or even improve while actual production economics deteriorate. This occurs when standard costs, inventory valuation methods, overhead allocations, or production assumptions fail to keep pace with operational reality. Commercial bankers who rely solely on reported margins may miss early signs of weakening earnings quality, cash flow […]

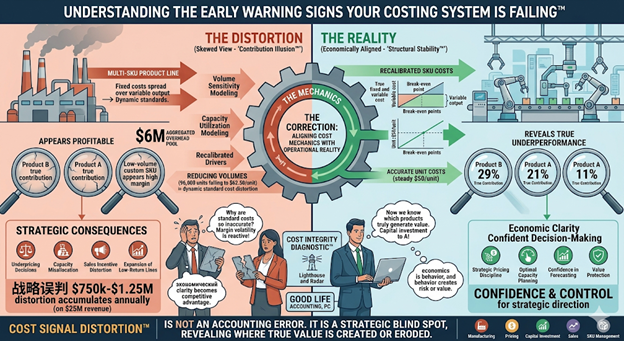

What Are the Early Warning Signs Your Costing System Is Failing?

Most costing systems don’t fail all at once—they drift. The challenge is that by the time the problem is obvious, the financial impact is already embedded in your margins, inventory, and pricing decisions. The early warning signs of a failing costing system include stable but misleading margins, recurring unexplained variances, frequent inventory adjustments, and growing […]

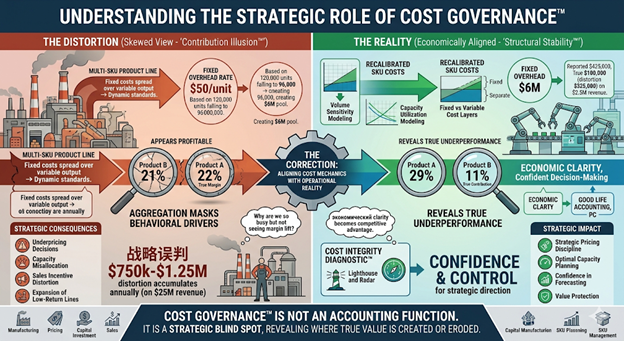

Why Do Manufacturing Cost Systems Drift Without Executive Cost Governance?

Manufacturing companies invest heavily in ERP systems, costing models, and financial reporting frameworks. These systems are designed to track materials, labor, overhead, and product margins with precision. However, as production environments evolve, the cost architecture that supports those reports often remains unchanged. Cost governance is the executive discipline of actively overseeing and periodically validating whether […]

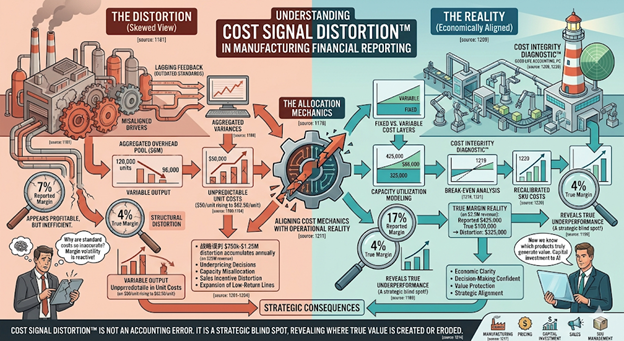

Why Do Manufacturing Cost Reports Sometimes Send the Wrong Signals?

Manufacturing leaders rely on financial reports to guide pricing decisions, production planning, capital investment, and product strategy. Margin analysis, SKU contribution reports, and variance reports are designed to translate operational activity into clear economic insight. Cost signal distortion occurs when internal financial reports appear precise but communicate misleading economic signals due to structural misalignment in […]

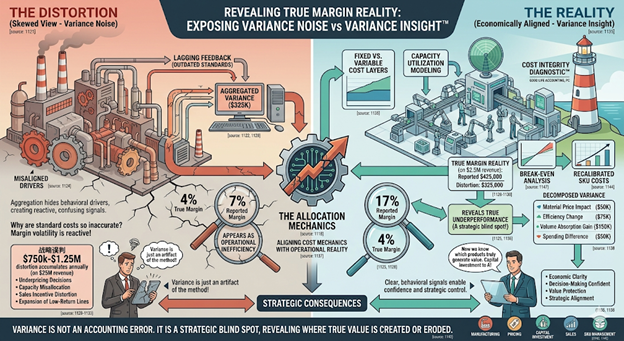

Why Do Manufacturing Variance Reports Stop Providing Useful Insight?

Manufacturing financial systems generate large volumes of variance data every month. Reports often include material price variance, labor efficiency variance, overhead spending variance, and production volume variance. In theory, these reports help management understand operational performance. Variance noise occurs when variance reports generate activity but not economic understanding. Instead of revealing meaningful changes in production […]

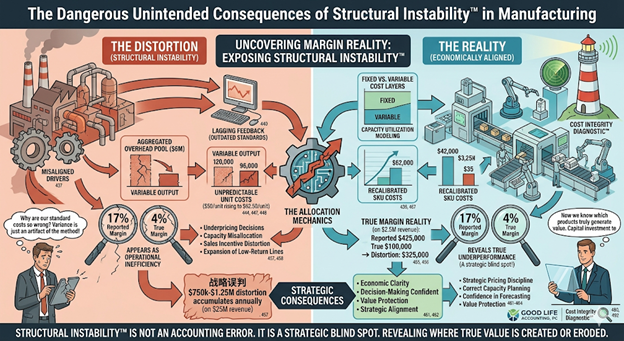

What Is Structural Instability in Manufacturing Cost Systems?

Every manufacturing company operates on an underlying cost structure that connects materials, labor, overhead, production flow, and volume behavior. This structure forms the foundation for pricing, margin analysis, and operational decision-making. Over time, however, businesses evolve while their cost systems often remain anchored to older assumptions. Structural instability occurs when a manufacturing cost system no […]