Do Small Inventory Adjustments Signal Bigger Problems for Manufacturing Lenders?

Direct Answer Yes. Small inventory adjustments often reveal larger operational, reporting, and collateral risks that may not yet be visible in financial statements. While a single inventory correction is usually not a concern, recurring inventory adjustments frequently indicate weaknesses in inventory controls, production reporting, transaction discipline, or inventory accuracy. For commercial bankers, the adjustment amount […]

Why Is Inventory Accuracy a Bigger Risk Than Most Commercial Lenders Realize?

Direct Answer Inventory accuracy is often a greater risk than inventory valuation because inaccurate inventory records can undermine borrowing base calculations, collateral coverage, gross margin reporting, and financial statement reliability long before inventory becomes obsolete or impaired. For commercial bankers, inventory problems typically begin as information problems, not valuation problems. When inventory records stop accurately […]

Why Do Inventory Problems Become ERP Problems?

Direct Answer Inventory problems become ERP problems because inventory is one of the most interconnected functions within a manufacturing business. Inventory touches purchasing, receiving, production, warehouse operations, shipping, costing, financial reporting, and customer service. When inventory processes are inaccurate, delayed, or inconsistent, the ERP system simply reports those problems more clearly. In most manufacturing ERP […]

When Does Manufacturing Inventory Become a Borrowing Base Risk?

Direct Answer Manufacturing inventory becomes a borrowing base risk when its recorded value no longer reflects its recoverable value. Inventory may appear accurate on financial statements while being impaired by obsolescence, aging, customer-specific requirements, inaccurate counts, or weak inventory controls. For commercial bankers, the most important question is not how much inventory exists—it is how […]

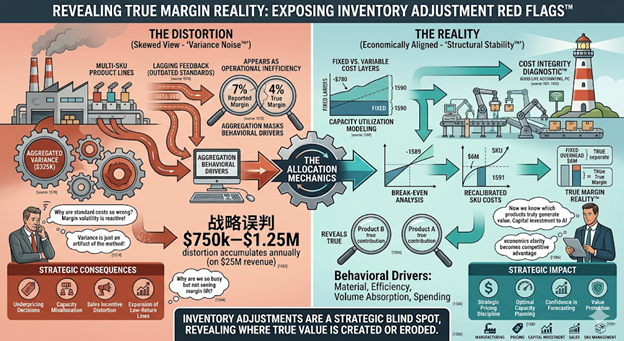

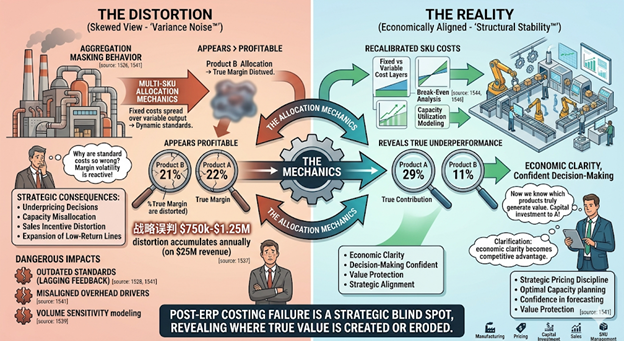

Why Are Inventory Adjustments a Cost System Red Flag (Not Just a Cleanup Issue?)

Inventory adjustments are often treated as routine accounting entries—something to fix discrepancies and move on. But that perspective misses the real issue. Inventory adjustments are not just corrections—they are signals. Frequent or unexplained adjustments indicate breakdowns in cost flow, transaction discipline, or system alignment, making them one of the clearest indicators that a costing system […]

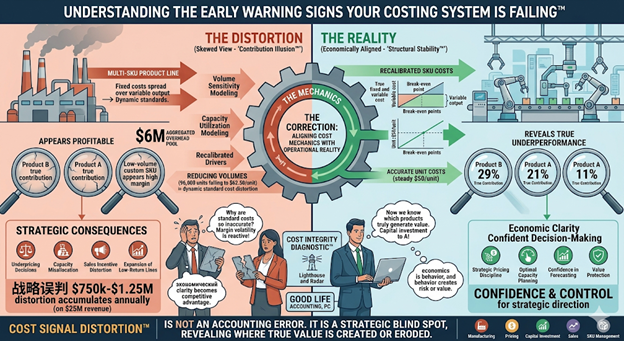

Why Do Variances Stop Being Useful (and What Does That Signal About Your Cost System?)

Variance analysis is supposed to be one of the most powerful tools in a manufacturing business. It highlights changes, surfaces issues, and drives corrective action. But in many companies, variances are still reported—yet no longer useful. Variances stop being useful when the underlying standards are no longer aligned with operational reality. When that happens, variances […]

What Are the Early Warning Signs Your Costing System Is Failing?

Most costing systems don’t fail all at once—they drift. The challenge is that by the time the problem is obvious, the financial impact is already embedded in your margins, inventory, and pricing decisions. The early warning signs of a failing costing system include stable but misleading margins, recurring unexplained variances, frequent inventory adjustments, and growing […]

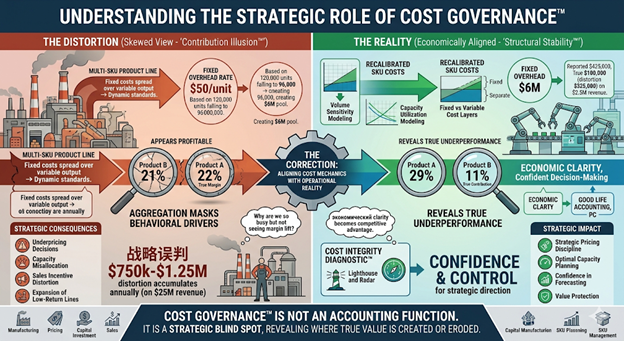

Why Do Manufacturing Cost Systems Drift Without Executive Cost Governance?

Manufacturing companies invest heavily in ERP systems, costing models, and financial reporting frameworks. These systems are designed to track materials, labor, overhead, and product margins with precision. However, as production environments evolve, the cost architecture that supports those reports often remains unchanged. Cost governance is the executive discipline of actively overseeing and periodically validating whether […]

Why Do Inventory Valuation Errors Create Lending Risk for Manufacturers?

For many manufacturing companies, inventory serves two roles at the same time. It is both an operational asset supporting production and a financial asset supporting working capital financing. Banks often lend against inventory balances through borrowing base structures that assume the reported values are reliable and economically aligned with production activity. Inventory collateral risk occurs […]

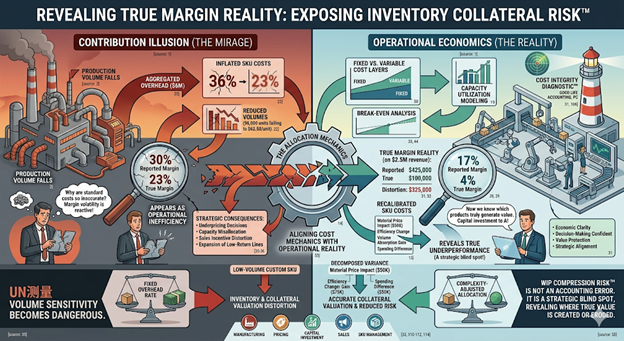

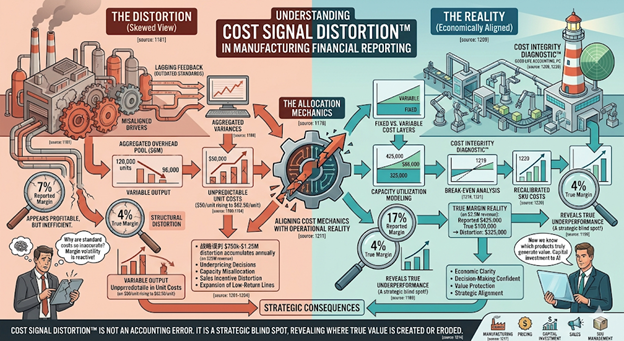

Why Do Manufacturing Cost Reports Sometimes Send the Wrong Signals?

Manufacturing leaders rely on financial reports to guide pricing decisions, production planning, capital investment, and product strategy. Margin analysis, SKU contribution reports, and variance reports are designed to translate operational activity into clear economic insight. Cost signal distortion occurs when internal financial reports appear precise but communicate misleading economic signals due to structural misalignment in […]